|

| A French Rock Star?? |

The political response to this evaporation of demand has, in the main, been to further reduce demand by cutting government expenditure and regulating the banks so that they are unable to lend money to would be investors, a result of the new capital adequacy rules. All of this has added further to the massive reduction in demand! Some argue that it has been necessary, the hawks tell us that growth and prosperity can only return when the “deleverage” is complete and they held sway in the early days of the Great Recession. More recently the Keynesians, ably led by Larry Summers and Paul Krugman have implored governments to throw caution to the wind and pour money into this black hole of aggregate demand with increased government investments and spending (and debt). There is a lot of angst between these two groups the Keynesians believe that huge capacity has been wasted unnecessarily and the hawks point to austerity in the US, UK and Spain as proof that recovery can only come when debts have been reduced to a manageable level. Piketty, who only joined the fray in 2014 is offering a more dramatic approach, which although not evoking the guillotine would nevertheless murder the savings of super wealthy people.

Gavyn Davies, who sits right in the middle of these camps, believes that this shortfall in demand is going to become a thing of the past in the US. As consumer spending in the US and UK drives growth there will increasingly be a more nature balance between supply and demand. He tells us that “this will be a year in which excess capacity in the global economy will start to be absorbed”.

|

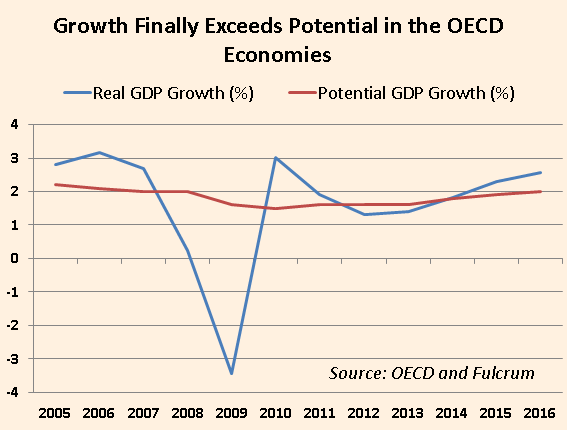

| Gavyn's Chart |

Add to this improving picture the recent drop in oil prices, that could add as much as 1% GDP growth to some developed economies, and we are at a tipping point. This is by no means true across the board, whilst the Anglo Saxon economies look likely to see capacity dwindle away, many developed economies in the EuroZone will still be in stagnation mode for a while. Mr Davies goes on to tell us that “Overall, then, economic performance in 2015 is likely to be a walk on the demand side. The supply side is showing no sign whatever of any improvement but, outside the US, that is still a long way from being the binding constraint on output”.

The question is, how will this play out in a highly globalised world? If, for arguments sake, demand becomes constrained in the US and UK during 2015 will these constraints manifest themselves in the normal way, through inflation and an up-tick in investment or will the threats that over-hang the rest of the world’s economies , of which deflation in the EuroZone is only one, mean that normal interactions might be suspended. Could inflation remain benign, investment weak and productivity low, as owners of capital continue to gravitate towards financial assets rather than new investments in productive capacity? Does the fact that so much wealth is now tied up in the hands of the old or very old mean that investment risk appetite is permanently damaged and that we have to, as Piketty tells us, tax these deal pools of wealth to get the money back into circulation

The answer to all this is almost certainly NO! I don’t have an equation that proves this but I don’t think I need one – normal service WILL BE RESUMED! Any way let’s hope so!

No comments:

Post a Comment